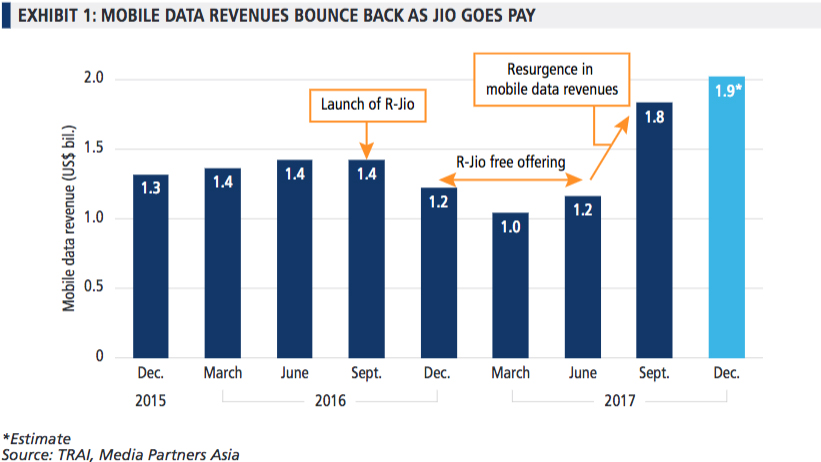

India’s telcos are looking more sure-footed these days as they recover from last year’s free data blitzkrieg orchestrated by deep-pocketed disruptive new entrant, Reliance Jio. Now Jio has gone pay, mobile data revenue growth has bounced back (click here for chart), restoring strategic confidence to telco majors. This uptrend should continue, especially as incumbents migrate to Voice over LTE (VoLTE), a response to Jio’s offer of free calls for life.

As broadband economics firm up, telcos are ramping up investment in fixed networks as well. In contrast to traditional pay-TV and telco businesses, willingness to pay for home broadband remains high, with demand for internet access surpassing data caps set on mobile plans.

Fixed broadband returns are looking promising as a result. While capital constraints and barriers to last mile access have inhibited growth in the past, new access technology like G.hn could smooth the way forward. At the same time, more robust fixed broadband infrastructure will help usher in 5G, although commercial services are only likely to launch in India by 2022 at the earliest.

It all adds up to a solid foundation for development and growth. Total data revenues in India are poised to reach ~US$20 bil. by 2022, expanding at a ~20% CAGR from 2017, and reshaping growth opportunities around media and communication in the process.

The latest issue of India Intelligence & Insights, from MPA India, looks at on-ground broadband trends that are often overlooked, and the impact they will have across the value chain.

HIGHLIGHTS

To find out more, please get in touch with Lavina Bhojwani

Vice President, India

Thank you for submission

Once you activate the account, your subscription entitles to receive 3 months of complimentary access to ‘The Digest’, MPA’s monthly email analysis,updates across TMT with exclusive industry interviews and data.

{kind=link}